The Kisan Credit Card scheme continues to play a central role in strengthening farmers’ access to institutional credit in India, enabling millions of cultivators and allied sector workers to obtain timely and affordable financing for agricultural activities. The initiative, which has evolved significantly since its launch in 1998, now supports a wide range of farming operations and allied activities while promoting financial inclusion in rural areas.

Agriculture and allied sectors remain the backbone of India’s rural economy, with nearly 46.1 percent of the country’s population dependent on farming, fisheries, animal husbandry and related activities for their livelihood. Ensuring reliable access to institutional credit has therefore remained a key policy priority for the government. In this context, the Kisan Credit Card scheme has emerged as one of the most significant financial instruments supporting farmers by simplifying credit access and reducing dependence on informal lenders.

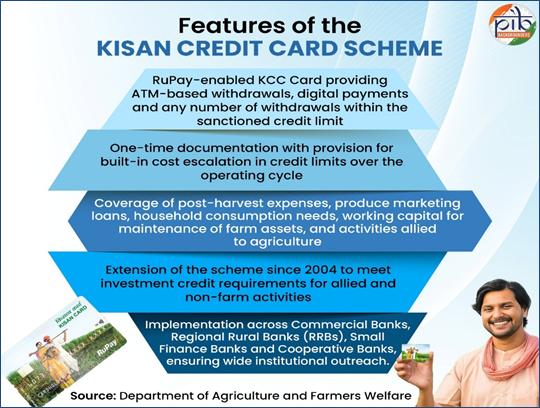

The revised Kisan Credit Card framework, introduced in 2020, expanded the scheme’s scope to provide integrated credit support covering short term crop cultivation, post harvest activities, marketing related expenses, farm maintenance and working capital requirements for allied sectors. The scheme also allows limited credit for household consumption needs and small investments related to farming.

Under the scheme, farmers are provided with a RuPay enabled credit card that allows flexible withdrawals, digital transactions and simplified documentation. This card functions as a revolving credit facility that enables farmers to draw funds whenever required within the sanctioned credit limit, ensuring continuous financial support throughout the agricultural cycle.

To make credit more affordable, the government introduced the Modified Interest Subvention Scheme as a central sector initiative in 2006–07. The scheme enables farmers to access short term crop loans at subsidized interest rates and provides incentives for timely repayment.

In the financial year 2025–26, the government further strengthened the scheme by enhancing the Kisan Credit Card lending limits. The crop loan limit under the Modified Interest Subvention Scheme has been increased from ₹3 lakh to ₹5 lakh. In addition, the credit limit for fisheries and allied agricultural activities has also been raised from ₹2 lakh to ₹5 lakh.

Another major reform introduced from 1 January 2025 is the increase in the collateral free credit limit from ₹1.6 lakh to ₹2 lakh per borrower. These changes are aimed at expanding access to institutional credit, particularly for small and marginal farmers who often face difficulties in securing formal loans.

Short term agricultural loans of up to ₹3 lakh under the scheme are currently available at an interest rate of 7 percent. Farmers who repay their loans on time receive an additional 3 percent interest subvention, reducing the effective interest rate to only 4 percent. This makes the Kisan Credit Card one of the most affordable agricultural credit instruments available to farmers.

The scheme covers a broad range of beneficiaries in order to ensure equitable access to institutional credit across the farming community. Eligible beneficiaries include individual farmers and joint borrowers who are owner cultivators, tenant farmers, oral lessees and sharecroppers.

The scheme also extends coverage to Self Help Groups and Joint Liability Groups, including those formed by tenant farmers and sharecroppers. This inclusive design ensures that even farmers without formal land ownership can access institutional credit.

To simplify the application process and expand outreach, a one page Kisan Credit Card application form has been introduced. The form includes basic applicant details that can be pre filled from PM KISAN records maintained by banks. Farmers are required to provide copies of land records and details of crops cultivated.

The simplified application form is widely distributed through national newspaper advertisements and is also available for download on the websites of scheduled commercial banks, the Department of Agriculture and Farmers Welfare and the PM KISAN portal. Common Service Centres have also been authorised to assist farmers in completing applications and digitally transmitting them to banks, ensuring easier access in remote rural areas.

In order to modernise the implementation and monitoring of the scheme, the government launched the Kisan Rin Portal in September 2023. The portal serves as a unified digital platform integrating farmer profiles, loan disbursement records, interest subvention claims and performance monitoring of the scheme.

For farmers, the portal provides simplified access to low cost institutional credit and supports coverage of allied sectors such as dairy farming, poultry, fisheries and beekeeping. It also enables faster loan processing through seamless digital integration between banks, cooperative institutions and government systems.

For banks and lending institutions, the portal facilitates automated submission and processing of interest subvention and prompt repayment incentive claims. The end to end digital framework reduces delays, improves transparency and enhances accountability in claim verification and settlement.

The Kisan Credit Card scheme has achieved extensive national coverage over the years. Currently, more than 7.72 crore Kisan Credit Cards are operational across India, with outstanding credit amounting to approximately ₹10.2 lakh crore. This reflects the scheme’s significant contribution in expanding institutional credit access for farmers and supporting agricultural productivity.

The credit delivery system under the scheme is supported by a broad institutional network. A total of 457 banks are onboarded on the Kisan Credit Card platform, including 37 commercial banks, 46 regional rural banks and 374 cooperative banks. This diverse banking network ensures widespread geographical coverage and efficient credit delivery at the grassroots level.

Across these institutions, more than 1,998.7 lakh Kisan Credit Card applications have been processed. Of these, 631.5 lakh applications were handled by commercial banks, 337.2 lakh by regional rural banks and 1030 lakh by cooperative banks. The data highlights the particularly important role played by cooperative banks in extending agricultural credit in rural areas.

The scheme has also been expanded to cover allied agricultural sectors in order to diversify income sources for rural households. In 2018–19, the government extended the Kisan Credit Card facility to fishers and fish farmers to support working capital requirements in fisheries and aquaculture activities.

The response to credit demand in allied sectors has been significant. In animal husbandry, 55.9 lakh applications were received, out of which 55.08 lakh were accepted and 39.22 lakh loans were sanctioned. This high acceptance rate reflects strong policy support and efficient screening mechanisms in the sector.

In the fisheries sector, 6.83 lakh applications were received and 6.77 lakh were accepted. A total of 4.82 lakh applications were sanctioned, indicating growing institutional credit access for fish farmers and aquaculture entrepreneurs.

The scheme has also played a major role in improving farm productivity by enabling timely investment in agricultural inputs such as seeds, fertilizers, irrigation systems and farm equipment. By providing affordable working capital, the scheme allows farmers to adopt improved farming practices and enhance crop yields.

The revolving credit facility provided under the Kisan Credit Card is valid for up to five years, enabling farmers to withdraw funds whenever required within the sanctioned limit. This flexibility helps align credit availability with agricultural production cycles.

Risk mitigation provisions have also been incorporated into the scheme. In cases of natural calamities, interest on loans may not be charged for up to one year and repayment periods can be extended up to five years in cases of severe disasters.

The scheme has proven particularly beneficial for small and marginal farmers, who hold approximately 76 percent of agricultural credit accounts under the Kisan Credit Card programme. By providing collateral free loans and concessional interest rates, the scheme significantly reduces barriers to accessing formal credit.

The government has also undertaken several initiatives to expand awareness and coverage of the scheme. Extensive information, education and communication campaigns are conducted in collaboration with state governments, the Reserve Bank of India, NABARD and banking institutions.

Under the Atmanirbhar Bharat Abhiyan, a nationwide Kisan Credit Card Saturation Drive has been launched to ensure that all eligible farmers, including those engaged in dairy, fisheries and animal husbandry, receive access to institutional credit. District level camps are organised regularly to facilitate the issuance of new Kisan Credit Cards.

The introduction of the RuPay enabled Kisan Credit Card has further strengthened digital financial inclusion in rural areas by enabling farmers to make digital payments and access funds through interoperable banking networks.

Officials stated that the Kisan Credit Card scheme has evolved into a comprehensive agricultural credit mechanism supporting cultivation, allied activities and post harvest operations within a single framework. With expanded credit limits, digital integration through the Kisan Rin Portal and broader sectoral coverage, the scheme continues to strengthen financial resilience in the agricultural sector.

The continued strengthening of the Kisan Credit Card programme is expected to play a crucial role in promoting sustainable agricultural growth, enhancing farmers’ incomes and supporting inclusive rural development across the country.